The One Big Beautiful Bill Act, enacted on July 4, 2025, has significantly altered American fiscal policy. For Canadian CPAs and accountants managing cross-border clients, grasping the new 2025 tax provisions is crucial. This comprehensive guide details every major change, and provides authoritative data.

Key Takeaways

- Permanently extends individual rate cuts first introduced under the TCJA Act while narrowing the gap between the highest and lowest brackets.

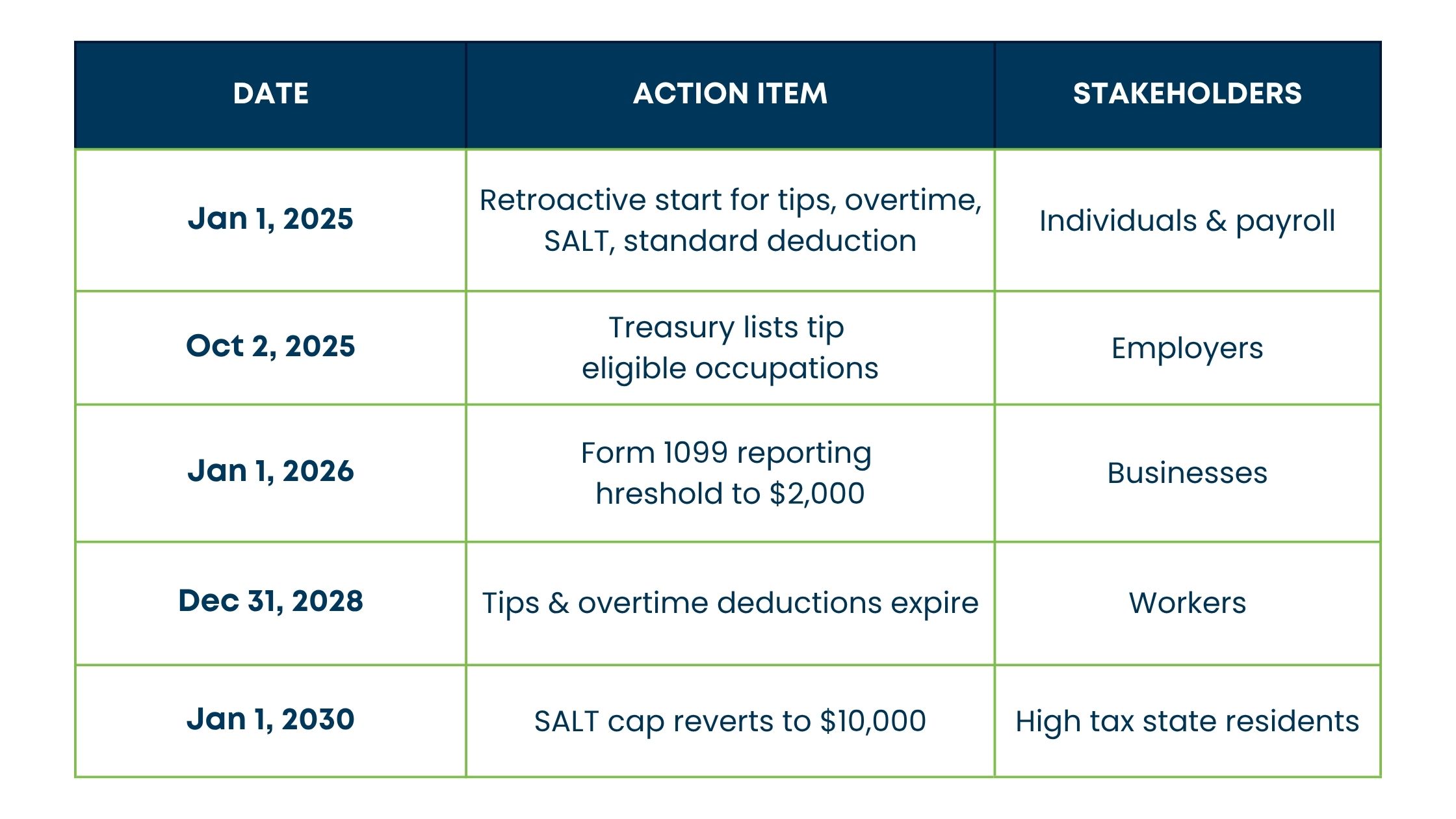

- Temporarily raises the SALT deduction cap to $40,000 for 2025-2029, phasing it out for MAGI above $500,000, before snapping back to $10,000 in 2030.

- Creates two unprecedented worker deductions, tips and overtime, capped at $25,000 each and available through 2028. To learn how NCS Global can help manage these changes, explore our Tax Services for cross border professionals.

- Lifts the standard deduction to $15,750 single / $31,500 joint for 2025 and locks in permanent inflation indexing thereafter. Nearly 90% of filers are expected to claim it, preserving the simplicity that taxpayers embraced after 2017.

- Makes 100% bonus depreciation and immediate domestic R&D expensing permanent, encouraging capital investment on U.S. soil.

- The plan is projected to add between $3.0 trillion and $3.4 trillion to the deficit from 2025 to 2034. However, it is also projected to boost long term GDP by 1.1% to 1.2%.

Why Canadian CPAs Must Act Now

Cross border taxpayers face a compressed timeline: many provisions are retroactive to January 1, 2025, and others sunset as early as 2028. Not aligning Canadian and U.S. filings properly could lead to double taxation or missed deductions. The following pages equip you with both the macro view and granular action steps.

Permanent Extensions of TCJA Individual Provisions

Locking In Rate Certainty

The TCJA Act trumps individual brackets that remain at 10%, 12%, 22%, 24%, 32%, 35%, and 37% through 2034. Permanency converts year to year guesswork into decade long planning clarity.

Standard Deduction Surge

For 2025 returns, the federal standard deduction rises to $15,750 single / $31,500 joint, an extra $750 and $1,500 respectively over 2024. The additional 65 plus “senior bonus” tacks on another $6,000 through 2028.

Because nearly 90% of filers already opt for the standard deduction, Canadian advisors should revisit U.S. housing and mortgage strategies for expatriate clients who formerly relied on itemising.

Revolutionary Worker Deductions

No Tax on Tips Deduction

- Eligible Workers: Occupations “customarily and regularly” receiving tips (Treasury list due Oct 2, 2025).

- Cap: $25,000 per filer.

- Payroll Note: FICA taxes still apply.

Overtime Premium Deduction

- Deduction equals the 50% premium portion of time and a half pay, capped at $12,500 single / $25,000 joint.

- Phaseouts start when Modified Adjusted Gross Income (MAGI) reaches $150,000 for single filers and $300,000 for joint filers.

For restaurants, hotels, and logistics firms with Canadian ownership but U.S. payrolls, immediate payroll system patches are essential to track deductible vs. FICA taxable amounts.

SALT Cap Reset: Five Year Golden Window

The SALT tax provision introduces a $40,000 cap from 2025-2029, indexed at 1% annually, reverting to $10,000 in 2030. Phaseout starts at 30% of income over $500,000, limiting high earners to a maximum deduction of $10,000. Effective marginal rates may exceed 45% for incomes between $500k and $600k.